Navigating The Hormuz Crisis And Its Impact On Global Economies

MIDDLE EAST CONFLICT

Iranians hold national flags beneath a large billboard reading "The Strait of Hormuz remains closed" as people gather in Tehran's Revolution Square after the United States and Iran agreed to a two-week ceasefire, on April 8, 2026.

Image: AFP

Hamza Ali Malik and Rupa Chanda

Washington and Tehran agreed to reach a two-week ceasefire and are expected to return to the negotiating table in Pakistan on April 10.

Although it's still unclear whether shipping through the Strait of Hormuz will resume, the recent repercussions highlight how a narrow stretch of water could send shock waves across the global economy.

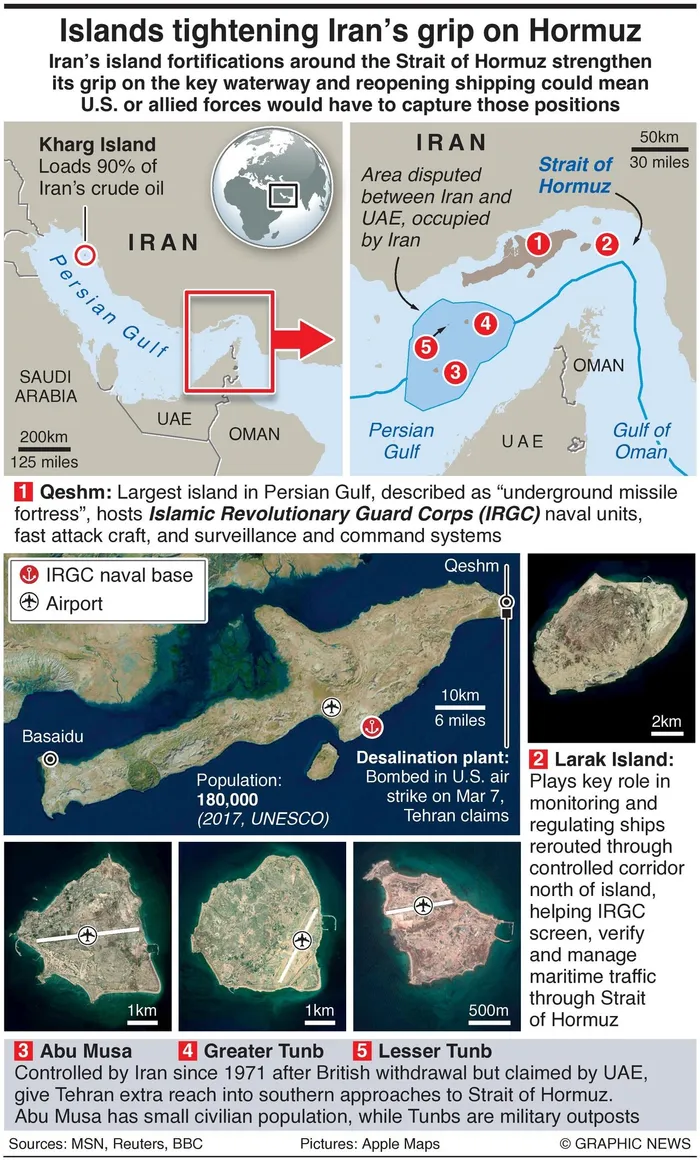

The Strait of Hormuz is the world's most critical energy choke point, with about one-fifth of global oil and LNG supply passing through it daily.

The conflict in the Middle East and the disruption of the strait have triggered what could become the region's most severe energy supply crisis in decades. But this isn't just an energy story. Economies are deeply interconnected today, and disruption in one region ripples across trade, transport, manufacturing, and even food security in other parts of the world.

During the days when tensions escalated, the region became a broader transport choke point. Iran sits at the centre of major regional transport networks, including the Asian Highways and Trans-Asian Railway. Critical highways and feeder corridors are affected, while rail links connecting Europe and Asia are under strain. Iran's maritime sector, one of the largest in the region, is also disrupted, amplifying the impact.

For landlocked developing countries, the stakes are higher. Many rely on Iranian ports for global market access. When operations are suspended at hubs such as Bandar Abbas and Chabahar, alternatives are limited and unreliable.

The first shock is energy. Countries such as Japan, the Philippines, the Maldives, Pakistan, the Republic of Korea, Singapore and several Pacific island economies depend heavily on crude oil imports from Gulf Cooperation Council countries, often sourcing over 50 per cent of their supply from GCC countries. When supply tightened and prices rose, the effect was felt instantly.

But the effect can extend far beyond energy. Asia-Pacific economies depend on complex global value chains, and disruption can cascade across sectors. Under these circumstances, high-tech industries face shortages of critical inputs like helium, essential for semiconductors and electronics.

Automotive production is affected by disruptions in naphtha, steel, aluminium, and bromine. Chemicals and fertilisers are becoming costlier and harder to source, threatening crop yields. Textile manufacturers face shrinking margins as polyester prices rise. Construction slows as materials like steel and cement become harder to transport.

Logistics is also under strain. Shipping diversions are adding 10 to 15 days to transit times, delaying critical goods from electric vehicle batteries to pharmaceuticals. Rerouting has created congestion at maritime hubs across Southeast and South Asia, risking wider instability across regional and global shipping networks.

Iran's stranglehold on the Strait of Hormuz

Image: Graphic News

The combination of logistics bottlenecks, supply shortages and depleting reserves could contract regional manufacturing if disruptions persist. What was once a well-functioning system is now under severe stress.

Beyond goods, the crisis has affected remittances and tourism. For many South Asian countries, remittances from GCC countries are vital. In Nepal, Pakistan, Sri Lanka and Bangladesh, about half of remittances originate there. India receives nearly a third, while in the Philippines, remittances account for 7.3 per cent of the GDP, with 17.8 per cent coming from GCC countries.

If GCC economies weaken due to the conflict, millions of Asia-Pacific migrant workers could be displaced.

Tourism is also taking a hit. Disruptions along Europe-Asia-Pacific routes and rising fuel costs are increasing airfares and reducing demand. The sector is reportedly losing around $600 million daily. Economies highly dependent on tourism, such as Fiji, the Maldives, Cambodia and Thailand (12.4 per cent), are particularly vulnerable.

Over the past days, oil prices rose by 45 per cent, gas by 55 per cent, and fertilisers by 35 per cent. Freight costs and insurance premiums are rising, increasing trade costs. As energy and commodity prices surge, many macroeconomic indicators are flashing red.

Financial markets are reacting with stock declines, currency depreciation and rising bond yields. Provisional ESCAP projections suggest headline inflation in developing Asia-Pacific could rise to 4.6 per cent in 2026, up from 3.5 per cent in 2025.

At the same time, growth is slowing. Higher energy costs, weaker trade and declining investor confidence are dragging economic activity. GDP growth for 2026 is projected at 4.0 per cent by ESCAP, down from 4.6 per cent in 2025 and well below the pre-pandemic average of 5.5 per cent.

The extent of impact on economies depends on their reliance on GCC oil and LNG, their trade and value chain linkages with Iran and GCC countries, their dependence on remittances and tourism for foreign exchange earnings, their energy reserves, alternative supply chains and their economic structure, particularly their reliance on energy-intensive industries.

If short-lived, impacts may remain contained with policy measures helping to stabilise economies. If prolonged without major infrastructure damage, the region may face a sustained slowdown, higher inflation and interest rates, weaker trade and investment, job losses, and rising debt vulnerabilities. It may also prompt a reassessment of energy security strategies.

But if energy and transport infrastructure are severely damaged, the consequences could be far more serious. Restoring infrastructure would take time, potentially triggering a global energy crisis, sustained logistics disruptions and a recession in the most affected economies.

While markets react quickly, the impact on humans unfolds more gradually but more deeply. Rising fertiliser costs are increasing food production costs, pushing up food prices and worsening food insecurity.

Poorer households, which spend a larger share of income on food, are the worst hit. Combined with slower growth, job losses, weak social protection, and declining remittances, this could lead to rising poverty and widening inequality across the region.

Economic interdependence is a double-edged sword. Asia-Pacific's integrated systems of trade, transport and energy have driven growth and efficiency but also created shared vulnerabilities. Disruptions in one part of the system can cascade rapidly across the region. This was evident during the COVID-19 pandemic.

The path forward is not retreating from economic interdependence, but making it more resilient. Led by domestic industrial and trade policies and supported by regional cooperation, diversification across the trade, transport and energy sectors, as well as sources, routes, products and markets, must become a priority to increase economic resilience.

At a strategic level, policymakers must balance growth with resilience. Reducing vulnerabilities should be as important as expanding output.

No country can navigate this alone. Regional cooperation platforms and mechanisms provided by ESCAP can help coordinate policy responses, share best practices and build long-term resilience.

From energy security to transport connectivity and trade facilitation to economic diversification, collective action will determine how effectively the region manages this crisis and prepares for future shocks.

What has happened in the Strait of Hormuz is a powerful reminder that in an interconnected world, distance offers no insulation. A regional conflict can quickly become a shared economic challenge, testing not just markets, but systems, policies and resilience itself.

* Hamza Ali Malik is the director of the Macroeconomic Policy and Financing for Development Division of ESCAP; Rupa Chanda is the director of its Trade, Investment and Innovation Division, and Weimin Ren is the director of its Transport Division. This article was originally published at https://www.chinadaily.com.cn/

** The views expressed do not necessarily reflect the views of IOL or Independent Media.